In the world of finance, time series forecasting using recurrent neural networks (RNNs) is a well-liked and effective method. I'll give an overview of RNNs' applications in finance for time series forecasting in this post, along with some Python code samples that make use of the TensorFlow library. We'll talk about the following subjects:

Introduction to Time Series Forecasting

A series of observations taken at regular intervals of time is called a time series. Time series data in finance can include economic indicators, stock prices, and exchange rates, among other things. Time series forecasting is the process of projecting future values using historical data. For many financial applications, including risk management, portfolio optimization, and stock market prediction, it is essential.

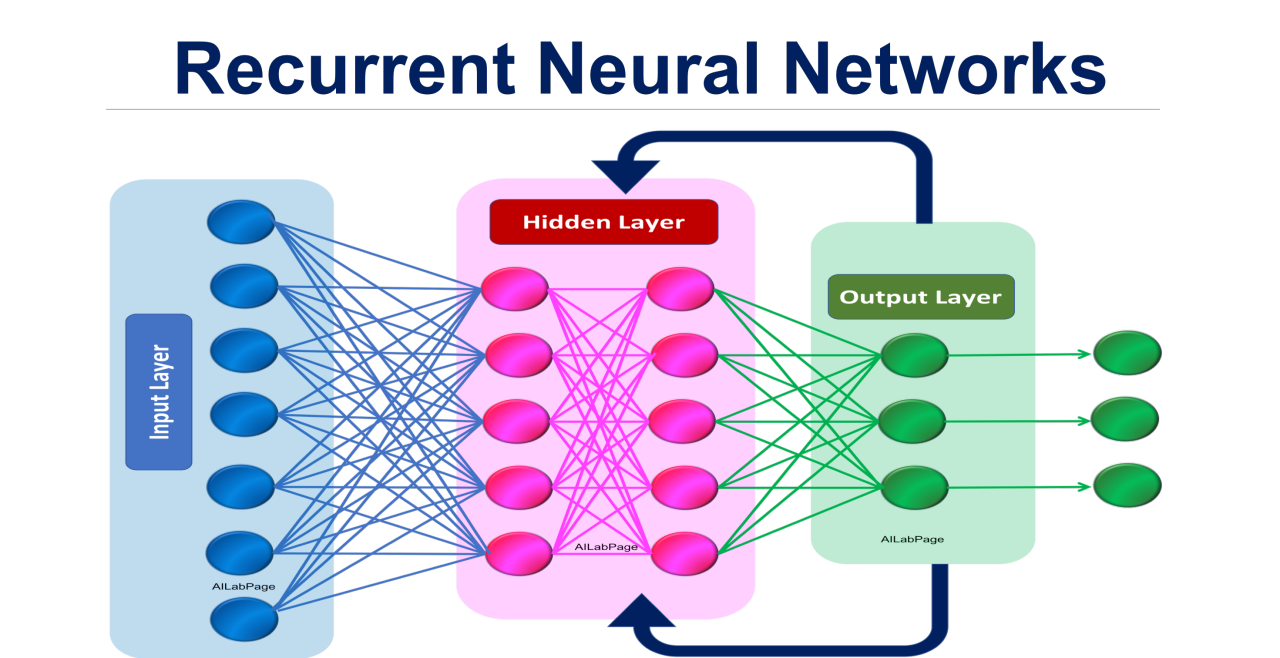

Recurrent Neural Networks (RNNs)

A particular kind of neural network called an RNN is made to process sequential data. They can gather data from earlier time steps because of an internal state. They can, therefore, identify patterns and dependencies in the data, which makes them ideal for time series forecasting.

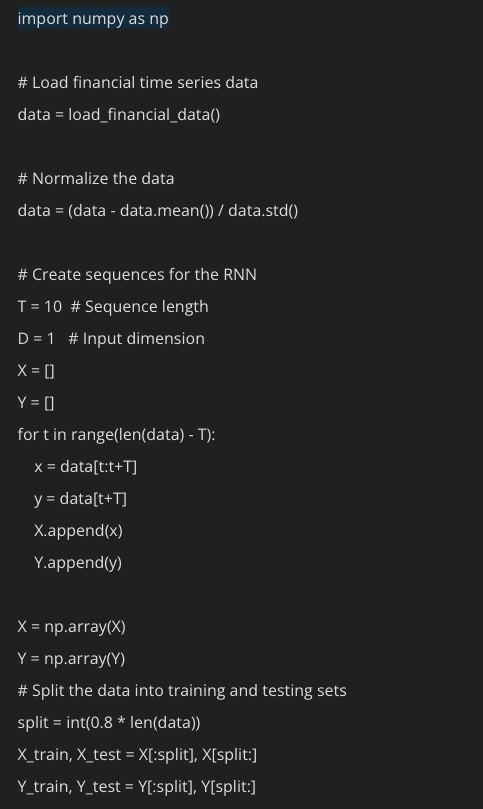

Data Preparation

It is necessary to prepare your financial time series data before constructing an RNN model. Usually, this includes:

A. Cleaning and loading the information.

B. Reshaping it to fit an RNN-appropriate format.

C. creating training and test sets for it.

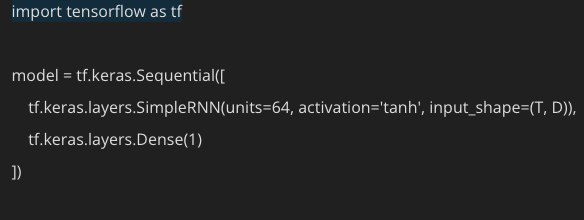

Model Architecture

We defined a simple RNN model with one RNN layer and one dense layer in the code snippet that was previously provided. To increase performance, you can play around with the architecture by introducing extra layers and modifying hyperparameters.

Model Training

The RNN model must be assembled and fitted to your training set of data to be trained. This is a sample of the code:

Analyzing the Model

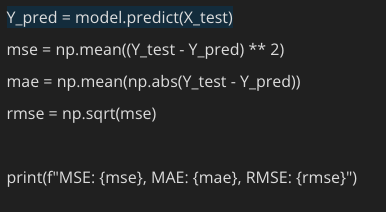

You should assess the model's performance using the testing data after it has been trained. Mean Squared Error (MSE), Mean Absolute Error (MAE), and Root Mean Squared Error (RMSE) are common evaluation metrics used in the finance industry for time series forecasting.

Conclusion

Recurrent neural networks (RNNs) in time series forecasting provide a potent tool for financial data analysis and prediction. Because RNNs can handle sequential data well, they are an excellent tool for tasks like portfolio optimization, risk management, and stock price prediction.

Financial time series data preparation, suitable RNN architecture definition, model training, and performance evaluation allow one to obtain important insights and make wise decisions in the ever-changing world of finance. To make accurate and trustworthy predictions in this intricate and unstable field, financial forecasting also needs domain expertise, meticulous data preprocessing, and continual model improvement.